Click to flip

By Zia Afzal

How Bitcoin

Fixed Money

A forensic diagnosis of money's structural pathology, tracing the erosion of the gold standard and the terminal decay of fiat. This book demonstrates how modern money, engineered as interest-bearing debt, embeds a mathematical impossibility at its core — one that violates the thermodynamic constraints governing all natural systems.

It examines not merely how Bitcoin functions, but why it works: as the first monetary architecture deliberately designed to restore equilibrium to an economic order structurally optimised for wealth extraction. The analysis moves beyond description into first principles, revealing the physics, mathematics, and incentive structures that underpin monetary stability.

The result is a clear and accessible exploration of the science behind Bitcoin's design — and the systemic failure it resolves.

Read The BookRead the Opening Pages

Select a chapter to preview its opening paragraphs, or open the full book viewer.

Preface

A generation ago, buying a home and raising a family on an average salary was an unremarkable achievement, the quiet expectation of a life lived by the rules. For those born after 1980, that same benchmark has become something closer to aspiration than expectation, a destination that recedes even as the effort intensifies. It’s a defining aspiration of a lifetime, and for most of today’s generation, one that remains permanently out of reach regardless of effort or sacrifice.

The deterioration did not announce itself. It accumulated slowly, almost politely, until the ordinary became extraordinary and the extraordinary became inaccessible. Wages erode in real terms while asset prices climb structurally beyond them. Debt expands faster than the productivity that is supposed to service it. The horizon of financial stability retreats faster than the capacity to advance toward it.

For the generation locked out of any realistic chance of achieving what their parents achieved, these circumstances often register as a personal shortfall, for some even a failing. They are in fact the result of architectural design. People are not failing, the system is not malfunctioning, nor is the situation a product of bad government or misguided policy choices that a better administration might reverse. The system is functioning precisely as its structure compels it to — and the structure itself is the problem. This is the direct and inevitable result of the architecture of modern money.

This book is written for those who wish to understand that architecture clearly — how incentives are structured, how purchasing power moves, and what alternatives might offer a way out of passive participation in a monetary system in which the finishing line, for most, is never reached.

Modern money is not an accident of history. It is a deliberately engineered system. Since 1971, when the last formal link between currency and gold was severed — ending centuries of physical backing — money has been created not through production, as it has been for millennia previously, but through debt. Currency can be created into existence from nothing, lent at interest, and reclaimed by the creator at the expense of the productive class with more than was issued because of the interest claimed at the moment of issuance.

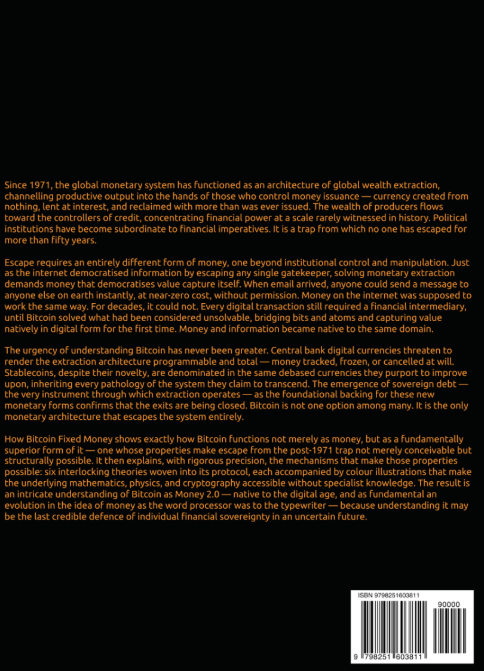

The mechanism is elegant. It concentrates power without visible coercion. Entire nations have been transitioned to debt-based money, and their populations charged a compulsory fee — interest camouflaged as inflation, to use their own money. Every transaction feeds the same machinery — the banking system. It transfers purchasing power gradually enough to avoid revolt, yet persistently enough to reshape society in just a generation.

Participation is not optional. Every salary, mortgage, pension, and contract is denominated within this structure. Every economic activity across the globe feeds it. Over time, the arrangement has normalised itself. Inflation is treated as natural. Debt is treated as inevitable. Each generation stands on a thinner economic foundation than the one before it yet doesn’t recognise the wealth dilution, obfuscated by manufactured economic theories of the day.

For over half a century, there has been no alternative or structural exit. Even for those who recognised the perpetual and insidious wealth extraction, there was no alternative. A trap set tight, forcing compliance and ensuring debt proliferation in every economy in the world.

A minority however, refused that settlement. Cryptographers, monetary theorists, and computer scientists recognised the structure and sought a way beyond it. The internet had already unshackled information—email dissolved the monopoly of the postal service, and ecommerce bypassed traditional retail gatekeepers. The question followed almost inevitably: could the digital revolution become the instrument that liberated money itself, freeing it from the extractive institutional trap.

For decades, the answer was no because digital information can be copied endlessly and money cannot survive duplication. Then in 2009, that problem was solved and the barrier broke.

For the first time in history scarcity was made possible in the digital realm. A digital unit that stored value and could not be copied was invented. Supply of it could not be altered at will. Ownership of it could be verified without an intermediary and it could be acquired by anyone without permission. The bridge between bits and atoms, between abstract software and economic reality was built. A new monetary organism had emerged.

The genesis of money 2.0 did not originate from a state, an academic institution, an economic think tank, or a bank. An unknown author released it and vanished. The code ran, the network survived and the system worked.

Bitcoin is not merely an asset. It is a structural challenge to the most powerful financial architecture ever constructed. Its design removes discretionary issuance. It eliminates the need for institutional trust. It converts energy directly into unforgeable units of value capture. It offers, for the first time in modern history, a monetary system that cannot be quietly diluted or have its issuance controlled by its custodians. The result is a monetary architecture resistant to capture and unusable as an extraction tool by a privileged few.

Understanding this shift matters. Monetary systems built on expansion and extraction eventually reach their limits. As debt compounds and wealth concentrates, productive economies strain. When expansion falters, the subsequent, almost inevitable contraction is abrupt: savings erode, currencies fracture, social cohesion weakens. History records this pattern repeatedly, and present-day conditions display the same symptoms.

Until now, there was no parallel system waiting in reserve—no independent monetary network capable of absorbing stress when the incumbent structure began to fail. When economies fractured in the past, populations were forced either into foreign currency systems or into informal barter. For the first time, a non-state monetary system exists that has already, in its brief history, acted as an alternative emergency rail in moments of crisis.

Understanding Bitcoin therefore is not about price predictions or timing its volatility or getting rich quick through making risky investments—it is about recognising a structural shift before it becomes impossible to preserve personal wealth in the current system. Understanding not only how it functions, but why it endures, is essential for anyone who wants to understand how the lifeboats will work while navigating the inevitable storm when it arrives.

This book exposes the machinery of modern money and describes how Bitcoin represents the first credible escape from it.

Table of Contents

Bibliography

[1]Acemoğlu, D., and Robinson, J. A. (2012). Why Nations Fail: The Origins of Power, Prosperity, and Poverty. Crown Business.

[2]Admati, A. and Hellwig, M. (2013). The Bankers' New Clothes: What's Wrong with Banking and What to Do about It. Princeton: Princeton University Press.

[3]Al-Bukhari, M. (9th century). Sahih al-Bukhari. Hadith on riba narrated by Ubada ibn al-Samit. Kitab al-Buyu (Book of Sales).

[4]Ammous, S. (2018). The Bitcoin Standard: The Decentralised Alternative to Central Banking. Hoboken, NJ: John Wiley & Sons.

[5]Ammous, S. (2018). 'Can Cryptocurrencies Fulfil the Functions of Money?' Quarterly Review of Economics and Finance, 70, 38-51.

[6]Ammous, S. (2021). The Fiat Standard: The Debt Slavery Alternative to Human Civilization. Saif House.

[7]Antonopoulos, A. M. (2017). Mastering Bitcoin: Programmeming the Open Blockchain (2nd ed.). O'Reilly Media.

[8]Aristotle. Politics, Book 1, Part X. Translated by Benjamin Jowett. Oxford: Clarendon Press, 1885.

[9]Atlantic Council (2023). 'The Bretton Woods Institutions Under Geopolitical Fragmentation.' GeoEconomics Centre Issue Brief.

[10]Ayub, M. (2007). Understanding Islamic Finance. John Wiley & Sons.

[11]Bank of England (2014). 'Money creation in the modern economy.' Quarterly Bulletin 54, no. 1: 14-27.

[12]Bretton Woods Conference (1944). Articles of Agreement of the International Monetary Fund. United Nations Monetary and Financial Conference.

[13]Brewer, J. (1989). The Sinews of Power: War, Money and the English State, 1688-1783. London: Unwin Hyman.

[14]Bureau of Labor Statistics (2024). 'Labor Productivity and Costs.' Economic News Release.

[15]Callen, H. B. (1985). Thermodynamics and an Introduction to Thermostatistics (2nd ed.). New York: John Wiley & Sons.

[16]Chapra, M. U. (1985). Towards a Just Monetary System. Leicester: Islamic Foundation.

[17]Chapra, M. U. (1992). Islam and the Economic Challenge. Islamic Foundation.

[18]CME Group (2017). Bitcoin Futures Contract Specifications and Trading Procedures. Chicago Mercantile Exchange Documentation.

[19]CoinMarketCap. Bitcoin market capitalisation data. Available at: https://coinmarketcap.com/

[20]Cordoba Capital Markets (2013). Private Placement Notes: Profit-Sharing Trade Finance. London Stock Exchange documentation.

[21]Cordoba Capital Markets (2020). 'SME Survey on Alternative Finance Preferences.' Internal research report.

[22]Cordoba Capital Markets (2024). Cross-Border Trade Financing via Profit Participating Notes. Investment Memorandum.

[23]Daly, H. E. and Farley, J. (2011). Ecological Economics: Principles and Applications (2nd ed.). Washington, DC: Island Press.

[24]De Roover, R. (1963). The Rise and Decline of the Medici Bank, 1397-1494. Cambridge, MA: Harvard University Press.

[25]De Roover, R. (1967). 'The Scholastics, Usury, and Foreign Exchange.' Business History Review 41.3: 257-271.

[26]De Soto, J. H. (2009). Money, Bank Credit, and Economic Cycles (3rd ed.). Ludwig von Mises Institute.

[27]Déroche, F. (2014). Qurʾans of the Umayyads: A First Overview. Leiden University Library.

[28]Eichengreen, B. (2008). Globalizing Capital: A History of the International Monetary System (2nd ed.). Princeton: Princeton University Press.

[29]El Diwany, T. (2010). The Problem with Interest (3rd ed.). London: Kreatoc.

[30]Eng, W. (2011). Trading with the COMEX: Gold and Silver Futures Markets. Wiley Finance.

[31]European Central Bank (2017). 'Base money, broad money and the APP.' Economic Bulletin, Issue 7.

[32]Fama, E. F. (1970). 'Efficient Capital Markets: A Review of Theory and Empirical Work.' Journal of Finance, 25(2): 383-417.

[33]Fama, E. F. and French, K. R. (1992). 'The Cross-Section of Expected Stock Returns.' Journal of Finance, 47(2): 427-465.

[34]Federal Reserve Bank of Chicago (1961). Modern Money Mechanics: A Workbook on Bank Reserves and Deposit Expansion.

[35]Federal Reserve Board (2024). 'What is the money supply? Is it important?' Frequently Asked Questions.

[36]Friedman, M. (1968). 'The Role of Monetary Policy.' American Economic Review, 58(1): 1-17.

[37]Friedman, M. and Schwartz, A. J. (1963). A Monetary History of the United States, 1867-1960. Princeton: Princeton University Press.

[38]GATA (Gold Anti-Trust Action Committee) (2010). Gold Market Manipulation: Evidence and Analysis.

[39]Gibert-Kochanowski, M. and Vonessen, M. (2021). 'Monetary financing and fiscal discipline.' Journal of International Money and Finance 117.

[40]Griffin, G. E. (1994). The Creature from Jekyll Island: A Second Look at the Federal Reserve. Westlake Village, CA: American Media.

[41]Hayek, F. A. (1944). The Road to Serfdom. University of Chicago Press.

[42]Hayek, F. A. (1976). Denationalisation of Money: The Argument Refined. Institute of Economic Affairs.

[43]Hull, J. C. (2017). Options, Futures, and Other Derivatives (10th ed.). Pearson.

[44]International Monetary Fund (2021). Asset Purchases and Direct Financing. IMF Departmental Paper.

[45]Iqbal, Z. and Mirakhor, A. (2011). An Introduction to Islamic Finance: Theory and Practise (2nd ed.). John Wiley & Sons.

[46]Irfan, H. (2015). Heaven's Bankers: Inside the Hidden World of Islamic Finance. New York: Overlook Press.

[47]Islahi, A. A. (1988). Economic Concepts of Ibn Taimīyah. Leicester: Islamic Foundation.

[48]Jorion, P. (2007). Value at Risk: The New Benchmark for Managing Financial Risk (3rd ed.). New York: McGraw-Hill.

[49]Kay, J. (2015). Other People's Money: The Real Business of Finance. New York: PublicAffairs.

[50]Kennedy, M. (1995). Interest and Inflation Free Money. Steyerberg: Permakultur.

[51]Keynes, J. M. (1936). The General Theory of Employment, Interest and Money. London: Macmillan.

[52]Khan, M. F. (1995). Essays in Islamic Economics. Islamic Foundation.

[53]Krugman, P. (2009). The Return of Depression Economics and the Crisis of 2008. New York: W.W. Norton.

[54]Kumhof, M. and Jakab, Z. (2016). 'The Truth about Banks.' Finance & Development, IMF, 53(1): 50-53.

[55]Kuran, T. (1986). 'The Economic System in Contemporary Islamic Thought.' International Journal of Middle East Studies 18.2: 135-164.

[56]Lane, F. C. (1973). Venice: A Maritime Republic. Baltimore: Johns Hopkins University Press.

[57]LBMA (2020). LBMA Precious Metal Prices and Forward Contracts. Market Documentation.

[58]Martin, F. (2013). Money: The Unauthorized Biography. Bodley Head.

[59]McLeay, M., Radia, A., and Thomas, R. (2014). 'Money Creation in the Modern Economy.' Bank of England Quarterly Bulletin, Q1: 14-27.

[60]Médecins Sans Frontières (2024). Access to Healthcare Under Siege: Gaza Situation Report. Geneva: MSF.

[61]Mises, L. von (1949). Human Action: A Treatise on Economics. Yale University Press.

[62]Murphy, C. & Comex Division (2015). Gold Futures and Options Trading Mechanisms. CME Group Market Regulation.

[63]Nakamoto, S. (2008). Bitcoin: A Peer-to-Peer Electronic Cash System.

[64]Nelson, B. (1969). The Idea of Usury: From Tribal Brotherhood to Universal Otherhood. University of Chicago Press.

[65]Nixon, R. (1971). Address to the Nation Outlining a New Economic Policy: 'The Challenge of Peace.'

[66]Nöldeke, T. et al. (2013). The History of the Qurʾān (W. H. Behn, Trans.). Brill.

[67]Office for National Statistics (2024). Housing Affordability in England and Wales: 2024. London: ONS.

[68]Oxfam International (2023). Survival of the Richest: How We Must Tax the Super-Rich Now to Fight Inequality.

[69]Page, B. I., Bartels, L. M., and Seawright, J. (2013). 'Democracy and the Policy Preferences of Wealthy Americans.' Perspectives on Politics, 11(1): 51-73.

[70]Palley, T. I. (2007). 'Financialization: What It Is and Why It Matters.' Working Paper No. 525, Levy Economics Institute.

[71]Perkins, J. (2016). Confessions of an Economic Hit Man (3rd ed.). San Francisco: Berrett-Koehler.

[72]Philippon, T. (2015). 'Has the US Finance Industry Become Less Efficient?' American Economic Review, 105(4): 1408-1438.

[73]Piketty, T. (2014). Capital in the Twenty-First Century. Harvard University Press.

[74]Popper, N. (2015). Digital Gold: Bitcoin and the Inside Story of the Misfits and Millionaires Trying to Reinvent Money. Harper.

[75]Quinn, S. (1997). 'Goldsmith-Banking: Mutual Acceptance and Interbanker Clearing in Restoration London.' Explorations in Economic History 34, no. 4: 411-432.

[76]Resolution Foundation (2023). The Housing Headwind: The Impact of Rising Housing Costs on UK Living Standards.

[77]Rickards, J. (2014). The Death of Money: The Coming Collapse of the International Monetary System. Portfolio/Penguin.

[78]Riksbank (2024). 'History of the Riksbank.' Sveriges Riksbank.

[79]Rothbard, M. N. (1962). Man, Economy, and State. Princeton: D. Van Nostrand Company.

[80]Rothbard, M. N. (2008). The Mystery of Banking (2nd ed.). Ludwig von Mises Institute.

[81]Ruggie, J. G. (1982). 'International Regimes, Transactions, and Change.' International Organization, 36(2): 379-415.

[82]Saez, E. and Zucman, G. (2020). 'The Rise of Income and Wealth Inequality in America.' Journal of Economic Perspectives 34, no. 4: 3-26.

[83]Sharpe, W. F. (1964). 'Capital Asset Prices.' Journal of Finance, 19(3): 425-442.

[84]Shiller, R. J. (2003). 'From Efficient Markets Theory to Behavioral Finance.' Journal of Economic Perspectives, 17(1): 83-104.

[85]Siddiqi, M. N. (2006). 'Islamic Banking and Finance in Theory and Practise.' Islamic Economic Studies, 13(2): 1-48.

[86]Small, K. (2011). 'Textual History of the Qur'an.' In The Qur'an: An Encyclopedia. Routledge.

[87]Spufford, P. (1988). Money and Its Use in Medieval Europe. Cambridge: Cambridge University Press.

[88]Stiglitz, J. E. (2012). The Price of Inequality. W.W. Norton & Company.

[89]Stiglitz, J. E. (2018). Globalization and Its Discontents Revisited. New York: W.W. Norton.

[90]Streeck, W. (2014). Buying Time: The Delayed Crisis of Democratic Capitalism. London: Verso.

[91]Taleb, N. N. (2007). The Black Swan: The Impact of the Highly Improbable. New York: Random House.

[92]Thiel, P. and Masters, B. (2014). Zero to One: Notes on Startups, or How to Build the Future. Crown Business.

[93]Treaty on the Functioning of the European Union (2012). Article 123 (Prohibition of monetary financing).

[94]Turk, J. and Rubino, J. (2013). The Money Bubble: What to Do Before It Pops. DollarCollapse Press.

[95]UNICEF (2024). The State of Food Security and Nutrition in the World 2024. Rome: FAO.

[96]Usmani, M. T. (1998). An Introduction to Islamic Finance. Idaratul Ma'arif.

[97]Visser, W. A. M. and McIntosh, A. (1998). 'A Short Review of the Historical Critique of Usury.' Accounting, Business & Financial History 8.2: 175-189.

[98]Vitali, S., Glattfelder, J. B., and Battiston, S. (2011). 'The Network of Global Corporate Control.' PLOS ONE 6, no. 10: e25995.

[99]Vogel, F. E. and Hayes, S. L. (1998). Islamic Law and Finance: Religion, Risk, and Return. Kluwer Law International.

[100]Vollset, S. E. et al. (2020). 'Fertility, mortality, migration, and population scenarios for 195 countries.' The Lancet 396, no. 10258: 1285-1306.

[101]Werner, R. A. (2014). 'Can Banks Individually Create Money Out of Nothing?' International Review of Financial Analysis, 36: 1-19.

[102]World Gold Council (2021). Gold Demand Trends: Full Year 2021. London: World Gold Council.

[103]Yaffe-Bellany, D. and Griffith, E. (2022). 'How Sam Bankman-Fried's Crypto Empire Collapsed.' The New York Times.

[104]Yang, L. (1952). Money and Credit in China: A Short History. Harvard University Press.

[105]Chaum, D. (1983). 'Blind Signatures for Untraceable Payments.' Advances in Cryptology: Proceedings of Crypto 82. Springer.

[106]Lamport, L., Shostak, R., and Pease, M. (1982). 'The Byzantine Generals Problem.' ACM Transactions on Programming Languages and Systems, 4(3): 382-401.

[107]Dai, W. (1998). 'b-money.'

[108]Szabo, N. (1998). 'Bit Gold.'

[109]Szabo, N. (2002). 'Shelling Out: The Origins of Money.'

[110]Back, A. (2002). 'Hashcash — A Denial of Service Counter-Measure.'

[111]Dwork, C. and Naor, M. (1993). 'Pricing via Processing or Combatting Junk Mail.' Advances in Cryptology — CRYPTO '92. Springer.

[112]Rivest, R. L., Shamir, A., and Adleman, L. (1978). 'A Method for Obtaining Digital Signatures and Public-Key Cryptosystems.' Communications of the ACM, 21(2): 120-126.

[113]National Institute of Standards and Technology (2015). Secure Hash Standard (SHS). FIPS PUB 180-4.

[114]Merkle, R. C. (1979). 'Secrecy, Authentication, and Public Key Systems.' Ph.D. Dissertation, Stanford University.

[115]Bachelier, L. (1900). 'Théorie de la Spéculation.' Annales Scientifiques de l'École Normale Supérieure, 3(17): 21-86.

[116]Mandelbrot, B. B. (1963). 'The Variation of Certain Speculative Prices.' Journal of Business, 36(4): 394-419.

[117]Einstein, A. (1905). 'Über die von der molekularkinetischen Theorie der Wärme geforderte Bewegung.' Annalen der Physik, 322(8): 549-560.

[118]Douceur, J. R. (2002). 'The Sybil Attack.' Proceedings of the 1st International Workshop on Peer-to-Peer Systems. Springer.

[119]Landauer, R. (1961). 'Irreversibility and Heat Generation in the Computing Process.' IBM Journal of Research and Development, 5(3): 183-191.

[120]Schneier, B. (1996). Applied Cryptography (2nd ed.). New York: John Wiley & Sons.

[121]Rogers, E. M. (2003). Diffusion of Innovations (5th ed.). New York: Free Press.

[122]Shor, P. W. (1994). 'Algorithms for Quantum Computation.' Proceedings of the 35th Annual Symposium on Foundations of Computer Science. IEEE.

[123]Grover, L. K. (1996). 'A Fast Quantum Mechanical Algorithm for Database Search.' Proceedings of the 28th Annual ACM Symposium on Theory of Computing.

[124]Shannon, C. E. (1948). 'A Mathematical Theory of Communication.' Bell System Technical Journal, 27(3): 379-423.

[125]Jevons, W. S. (1875). Money and the Mechanism of Exchange. London: Appleton.

[126]Kydland, F. E. and Prescott, E. C. (1977). 'Rules Rather than Discretion.' Journal of Political Economy, 85(3): 473-491.

[127]Cantillon, R. (1755). Essai sur la Nature du Commerce en Général. London: Fletcher Gyles.

[128]Radford, R. A. (1945). 'The Economic Organisation of a P.O.W. Camp.' Economica, 12(48): 189-201.

[129]Bernstein, P. L. (2000). The Power of Gold: The History of an Obsession. New York: John Wiley & Sons.

[130]Fergusson, A. (1975). When Money Dies: The Nightmare of the Weimar Collapse. London: William Kimber.

[131]Hanke, S. H. and Krus, N. (2013). 'World Hyperinflations.' In Routledge Handbook of Major Events in Economic History. London: Routledge.

[132]Hamilton, E. J. (1934). American Treasure and the Price Revolution in Spain, 1501-1650. Cambridge, MA: Harvard University Press.

[133]Friedberg, A. (2009). Paper Money of the United States (19th ed.). Coin & Currency Institute.

[134]Executive Order 6102 (1933). 'Forbidding the Hoarding of Gold Coin, Gold Bullion, and Gold Certificates.' Federal Register.

[135]Eichengreen, B. (2011). Exorbitant Privilege: The Rise and Fall of the Dollar. Oxford: Oxford University Press.

[136]Maddison, A. (2007). Contours of the World Economy, 1-2030 AD. Oxford: Oxford University Press.

[137]Caro, R. A. (2012). The Passage of Power: The Years of Lyndon Johnson. New York: Alfred A. Knopf.

[138]Cambridge Centre for Alternative Finance (2024). Cambridge Bitcoin Electricity Consumption Index. University of Cambridge.

[139]Bitcoin Mining Council (2024). Global Bitcoin Mining Data Review: Q4 2024.

[140]Visa Inc. (2024). 'Visa Fact Sheet.'

[141]Federal Reserve (2024). 'Fedwire Funds Service — Annual Statistics.'

[142]SWIFT (2024). 'SWIFT in Figures.'

[143]Bank for International Settlements (2024). 'CBDCs: An Opportunity for the Monetary System.' BIS Annual Economic Report.

[144]Atlantic Council (2024). 'Central Bank Digital Currency Tracker.' GeoEconomics Centre.

[145]Bureau of Labor Statistics (2024). CPI Inflation Calculator. US Department of Labor.

[146]Glassnode (2025). 'Bitcoin Exchange Balance.' On-Chain Market Intelligence.

[147]CVE-2018-17144 (2018). 'Bitcoin Core Denial of Service / Inflation Vulnerability.'

[148]99Bitcoins (2025). 'Bitcoin Obituaries.'

[149]Samuelson, P. A. (1948). Economics: An Introductory Analysis. New York: McGraw-Hill.

[150]Friedman, M. (1991). 'Island of Stone Money.' Working Papers in Economics, E-91-3. Stanford, CA: Hoover Institution.

[151]Grierson, P. (1991). Numismatics. Oxford: Oxford University Press.

[152]De Roover, R. (1948). Money, Banking and Credit in Mediaeval Bruges. Cambridge, MA: Mediaeval Academy of America.

[153]Moore, G. E. (1965). 'Cramming More Components onto Integrated Circuits.' Electronics, 38(8): 114-117.

[154]US Bureau of Engraving and Printing (2024). 'Annual Production Figures.'

[155]Vine, D. (2015). Base Nation: How U.S. Military Bases Abroad Harm America and the World. New York: Metropolitan Books.

[156]US Department of Defense (2024). 'Department of Defense Annual Energy Management and Resilience Report.'

[157]El Salvador Legislative Assembly (2021). 'Bitcoin Law (Ley Bitcoin).' Decree No. 57.

[158]US Securities and Exchange Commission (2024). 'SEC Approves Spot Bitcoin Exchange-Traded Products.'

[159]MicroStrategy Incorporated (2024). 'Form 10-K: Annual Report.' SEC Filing.

[160]European Central Bank (2023). 'A Stocktake on the Digital Euro.' Frankfurt: ECB.

[161]Bank of England (2023). 'The Digital Pound: A New Form of Money for Households and Businesses?' Consultation Paper.

[162]Stoll, C. (1995). 'The Internet? Bah!' Newsweek, 27 February 1995.

[163]Bank of England (2024). 'A Millennium of Macroeconomic Data.'

[164]Gresham, T. (1558). Letter to Queen Elizabeth I. Cited in Mundell, R. A. (1998).

[165]Peel, M. and England, A. (2020). 'Bank of England Refuses to Release Venezuela's Gold.' Financial Times.

[166]Central Bank of Nigeria (2021). 'Letter to All Deposit Money Banks.' CBN Circular.

[167]People's Bank of China (2021). 'Notice on Further Preventing and Disposing of the Risk of Virtual Currency Trading Speculation.'

Get Your Copy

Available in paperback and digital edition. Understand why Bitcoin is not a speculative asset, but a technological solution to a historical engineering problem.

Hardback

Coming Soon

The hardback edition — a permanent addition to your library. Register your interest and be the first to know when it launches.

Subscribe

£5/month

Full access to the book, plus exclusive tools built around it.

- The complete digital book with custom-built RSVP reader — elevate your reading speed from 250 wpm to 800 wpm

- All blog posts — Essays on Bitcoin, Essays on Money, and Papers

- AI Analyst — trained on the book, its 132-source bibliography, live crypto feeds, on-chain data, and social sentiment from X and Reddit

- Crypto Sources — 100+ curated feeds across macro-economics, protocol development, industry news, mining, price analytics, and Islamic finance

- Bitcoin Live — real-time mempool visualisation, on-chain metrics, fee tracking, and price charts

- Daily digests delivered to your inbox or Telegram

₿ Pay with Bitcoin — coming soon